🔑 Registre una cuenta con Gate.io

👨💼 Complete KYC en un plazo de 24 horas

🎁 Reclamar recompensas de puntos

Noticias cripto, titulares e información

In the crypto coin trading market, back-testing can be simply understood as our "retest" of past trading strategies. It is a valuable experience in user trading activities and a key step in optimizing investment strategies. Considerable income is the ultimate goal that traders always pursue. Effective use of the "historical wealth" from these backtests will help achieve higher income achievements.

As a practical function for exploring new trading strategies and new markets, backtesting can help investors use historical data and provide valuable trading strategy feedback. In Gate.io quantitative trading, no matter what kind of quantitative strategy for CTA signal tracking is formulated, backtesting can reduce strategy errors or capital investment risks, thereby improving the success rate of quantitative trading strategies.

What is backtesting

As the name implies, backtesting is based on different quantitative strategies and time periods set by the user. The backtest results will show complete transaction data under the strategy and time period, including total profit, maximum profit and loss, and maximum drawdown percentage. The user can conduct a back-test before executing the strategy, and use the back-test result as a reference to judge the feasibility of the strategy.

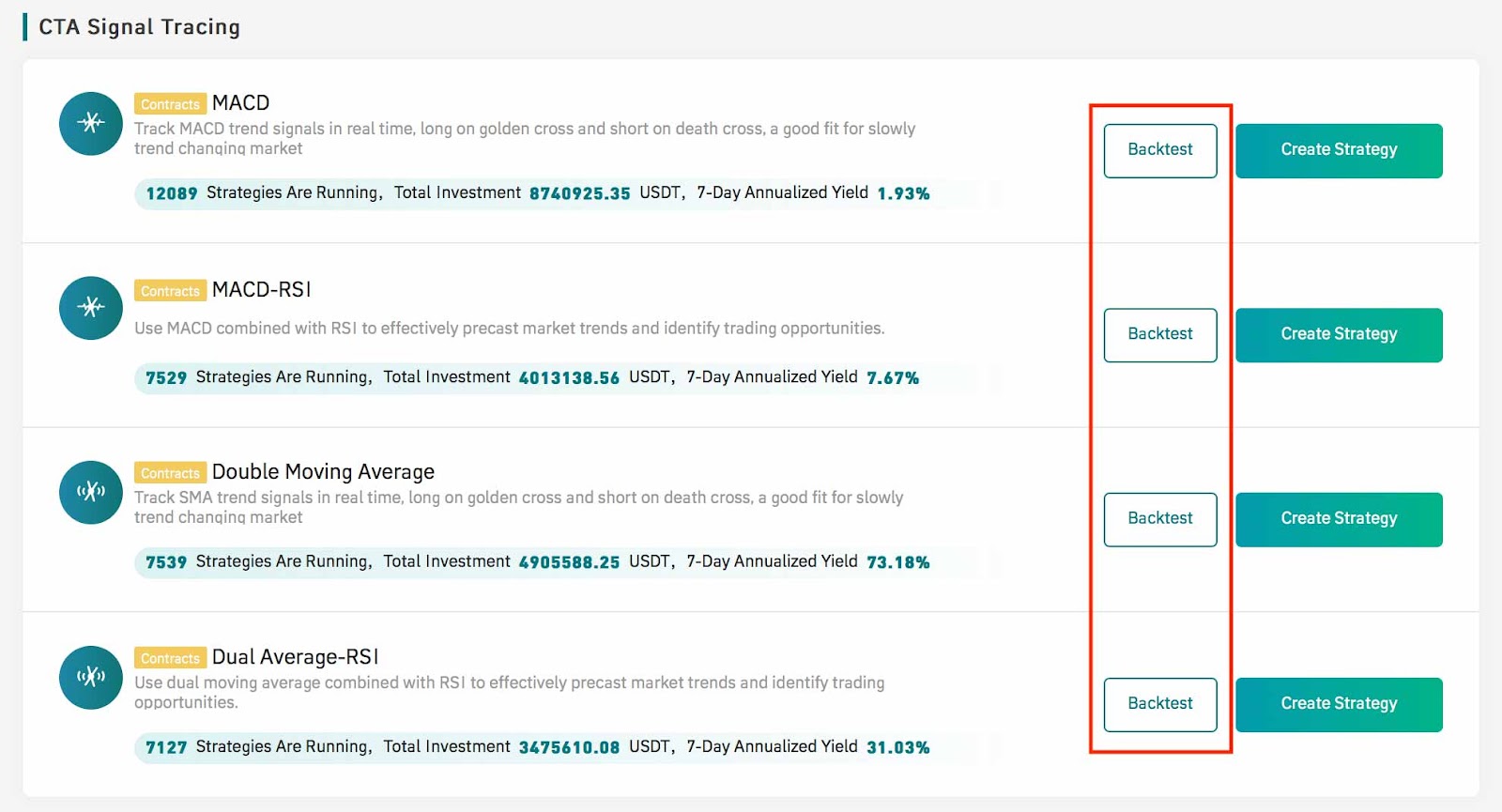

Gate.io quantitative trading strategy library includes six quantitative strategies: spot grid trading, contract grid trading, MACD (exponential smoothed moving average), double moving average, MACD-RSI, double moving average-RSI, users can freely choose to use, return The measurement function is currently applicable to CTA signal tracking strategies, that is, the last four quantitative strategies except grid trading.

For backtesting, there are two points to note here. First, if we understand the risks and potential benefits of a certain quantitative strategy through the backtesting function, this will greatly help the formulation of subsequent quantitative strategies, and it can also ensure that the quantitative strategy is in the actual trading market. The feasibility. It can be seen that the objective and true back-testing feedback data only needs our targeted optimization strategy to easily realize the benefits.

Another situation is that if we collect backtest results under a certain or extreme market situation, we need to carefully consider market changes and other factors. Quantitative strategy optimization based on such backtest data may result in further damage to earnings; therefore, the current market conditions in the implementation of quantitative strategies are critical to the impact of the strategy, and traders must always maintain a risk awareness of market conditions.

How to conduct a backtest

Find "CTA Signal Tracking" in the "Becoming Signal" column, and click the "Backtest" button after the corresponding quantitative strategy to perform the backtest.

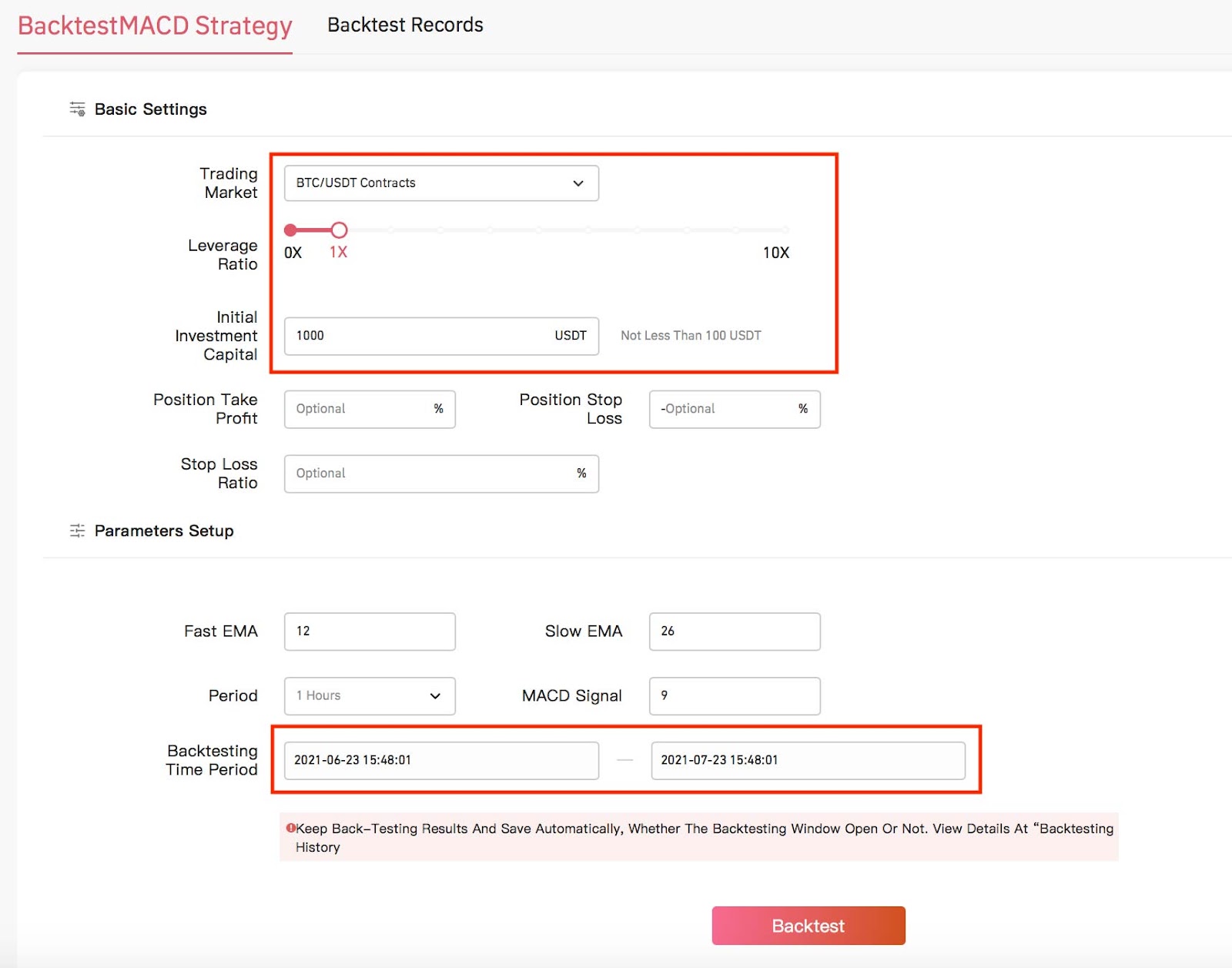

Fill in relevant information on the backtest strategy page, including trading market, leverage, initial investment, backtest time period, etc.

Then we will get some back-test data, including a profit and loss overview, back-test charts, and transaction records.

How the backtest works

Simply, the working principle of backtesting is to refer to valuable data in the history of the trading market to guide current or future trading strategies. The trading market is constantly changing. Finding historical data that is helpful to quantitative strategies is no easy task. Data in a short period of time cannot effectively "predict" the future market. This requires that the backtesting time must be a longer period of history. cycle.

Secondly, in order not to affect the strategic bias brought by historical data, traders need to maintain a rational judgment on the backtest data obtained. Misleading data may make quantitative strategies counterproductive. Before formulating a strategy, it is particularly important to ensure that the data obtained must be helpful to the strategy. When we rely on backtesting data to imagine possible situations and can effectively avoid misunderstandings, we can effectively use them.

A full understanding of the working principle of backtesting is the prerequisite for backtesting. At the same time, Gate.io's quantitative trading also provides a huge quantitative strategy library for the majority of novices and professional users, helping users to use various quantitative models to strictly conduct automatic, stable, and stylized transactions, and overcome the cognitive bias caused by manual judgment. As a built-in function of quantitative trading, backtesting is highly compatible with the working philosophy of quantitative trading.

The difference between backtesting and simulated trading

After understanding the working principle of backtesting, we will find that it has similarities with simulated trading. In fact, the data obtained from the backtest can be tested in a simulated disk, or it can be said to be a test of the back-test results, which helps the formulation of quantitative strategies to some extent. However, occasional test success or failure does not negate the reason for the backtest function, because there is no absolute accuracy in predicting future market conditions.

Under normal circumstances, users will be provided with simulated disks to operate and familiarize themselves with the product before the new product goes online. There are many benefits of simulated trading, such as saving money, judging trends, trading practice, etc. In simulated trading, users can trade based on many of the same functions provided as real orders without investing real money, which is an excellent channel for optimizing strategies and understanding products.

The essence of backtesting is to provide a relatively valuable trend and data reference for the future. If you blindly use backtesting data for simulated trading, it is actually very unfriendly to improve the trading ability of traders. Investors rely on backtesting data to repeatedly formulate and optimize quantitative trading strategies which is key to improving their trading capabilities. Steadily increasing returns are also generated in every real transaction. This is also the value of backtesting.

Summarize

With the rise of quantitative trading, more and more investors have created a lot of benefits by relying on the detailed data analysis of the backtest function, comprehensive backtest dimensions, and real-time strategy evaluation. They have become "signalers" before they formulate strategies. "Military-level" auxiliary tools. Of course, the backtesting function is not a perfect tool for strategy development. The backtesting data naturally contains the trader’s past "bias" information. The scientific and reasonable use of the backtesting function can help investors refine their trading strategies and achieve sustainable quantitative trading income.

🔑 Registre una cuenta con Gate.io

👨💼 Complete KYC en un plazo de 24 horas

🎁 Reclamar recompensas de puntos